CCTV News:On May 13th, the People’s Bank of China, the Hong Kong Securities Regulatory Commission and the Hong Kong Monetary Authority announced the launch of a number of "cross-connect" business optimization measures to better meet the diversified risk management needs of domestic and foreign investors and reduce participation costs.

This optimization has improved and upgraded many functions and supporting services of InterchangeLink, including adding standardized interest rate swap contracts with the settlement date in the international money market as the payment cycle, launching contract compression services, optimizing related system functions, and extending the preferential period of fees.

News link: What is "Interchangeable Link"

What is "Interchangeability"? "Exchange Link" is a mechanism arrangement created for foreign investors to manage interest rate risk after purchasing various RMB assets including bonds through channels such as "Bond Link", which is mainly used to manage the risk of RMB interest rate fluctuation.

"Exchange Link" has solved the problems of inconvenience and high cost for foreign investors to carry out RMB interest rate risk management before, which is helpful to attract more international investors to participate in the China bond market and further enhance the confidence of foreign investors in holding RMB assets such as bonds.

Lu Xiangqian, general manager of the Second Market Department of China Foreign Exchange Trading Center, said that "Exchange Link" and "Bond Link" will cooperate with each other to further release the potential of overseas investors to invest in the mainland capital market, which will help to enhance the depth and breadth of the national financial market and promote the internationalization of RMB.

There are 58 foreign institutional investors who have entered the market through the "Exchange Link".

Since the launch of "Interchangeable Connect" in May 2023, the cumulative number of overseas institutional investors of "Interchangeable Connect" has reached 58. At the same time, its transaction volume has also increased steadily, and the types of covering institutions have been increasing.

The data shows that from May 2023, when the "Interchangeable Connect" was launched, to the end of April 2024, the cumulative number of overseas institutional investors in the "Interchangeable Connect" reached 58, including commercial banks, securities companies, asset management companies and other types of qualified institutional investors, covering more than ten countries and regions. The accumulated transactions exceeded 1.77 trillion yuan, and the daily average transaction clearing volume increased steadily from less than 3 billion yuan in the first month of launch to more than 12 billion yuan in April 2024. In the same period, the balance of custody of overseas institutional investors in the China bond market increased by nearly 800 billion yuan.

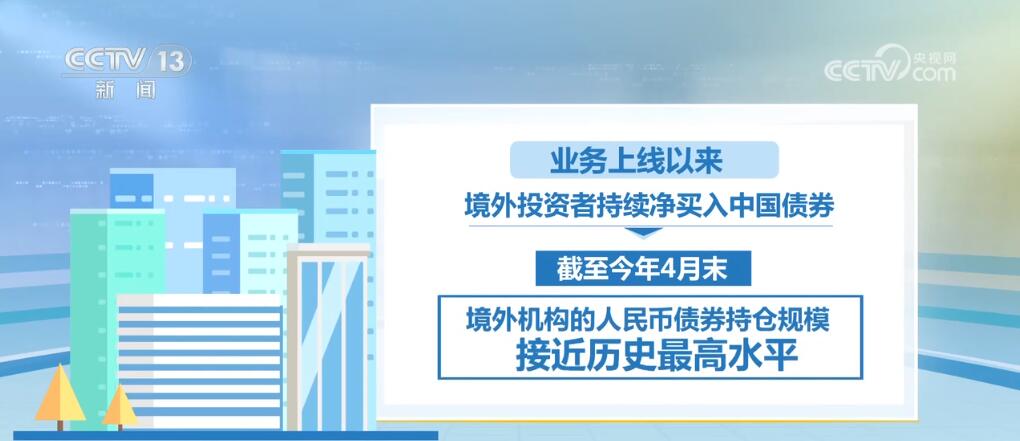

Foreign investors continue to buy China bonds in a net way.

Then why should the "Interchangeable Connect" introduce optimization measures? It is understood that the "Interchangeable Link" has previously opened the "Northbound Interchangeable Link", that is, overseas investors from Hong Kong and other countries and regions participate in the inter-bank interest rate swap market in the Mainland through infrastructure interconnection between the two places.

Since the launch of the business, foreign investors have continuously bought China bonds in a net way. By the end of April this year, the scale of RMB bond positions held by overseas institutions was close to the highest level in history.

With the expansion of foreign investors’ debt holding scale and the increase of trading activity, foreign investors have proposed that they hope that "InterchangeConnect" can launch more transaction clearing services in line with mature international markets to help investors better manage risks. This optimization measure is aimed at these actual needs.

Cheng Leilei, general manager of Business I of Shanghai Clearing House, said that this time, the interest rate swap contract was launched in line with the practice of settlement date in the international money market, and a fixed payment cycle unified with the international market was adopted, so that funds were received and paid only on four fixed settlement dates every year, which greatly reduced the difficulty of internal transaction management of overseas institutions, and was conducive to linking interest rate swap transactions carried out by overseas institutions in different countries and facilitating their risk management. In addition, other system optimization and preferential measures have been introduced this time, which will help to better meet the diversified risk management needs of investors and reduce the participation cost.

It is expected that more derivatives will be included in the "Exchange Link"

Experts said that with the launch of this series of optimization measures, it is expected that the scale and participants of "Interchangeable Connect" transactions will continue to increase in the future.

Lu Xiangqian said that with the continuous increase in the scale of RMB assets held by foreign investors and the launch of this series of optimization measures, it is expected that the scale and participants of "Interchangeable Connect" transactions will continue to increase in the future. In the next step, China Foreign Exchange Trading Center will continue to cooperate with other financial infrastructure to study the inclusion of more domestic interest rate derivatives in the "Interchangeable Link" framework.

At the same time, the "Exchange Link" will help promote the coordinated development of financial markets in the Mainland and Hong Kong, build a high-level financial opening pattern, and support the consolidation and promotion of international finance centre’s status.

Cheng Leilei said that the Shanghai Clearing House and the innovative mechanism of the cooperative institutions have realized the integrated arrangement of transaction clearing. In many aspects such as agreement rules, market entry transactions, clearing and settlement, risk management, etc., the difficulty and complexity of domestic and foreign investors’ participation are reduced, which provides a more convenient and efficient channel for domestic and foreign investors to participate in the financial derivatives markets of the two places. This is conducive to further strengthening the in-depth cooperation between Hong Kong and the mainland financial markets and promoting the healthy and stable development of the financial markets of the two places.

关于作者